SELAMAT DATANG DI ONGTOTO ( MOHON USERNAME DAN PASWORD TIDAK DISAMAKAN UNTUK MENJAGA KEAMANAN AKUN )

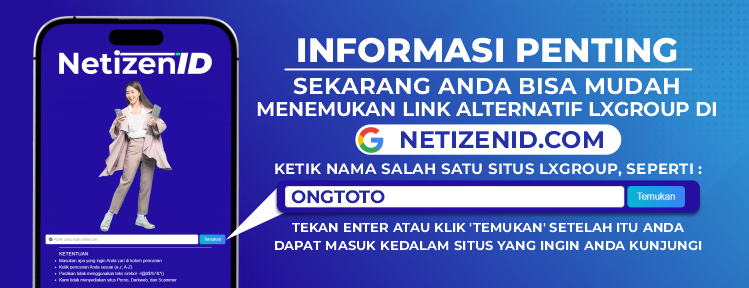

LINK ALTERNATIF : https://netizenid.com/

CONTOH : masukan keyword ONGTOTO dan klik temukan maka akan muncul link alternatif yang aktif.

========================================

PERHATIAN!!!

Untuk semua member ONGTOTO yang melakukan deposit harap untuk TIDAK menuliskan BERITA keterangan apapun pada kolom berita transfer bank.

Untuk member yang transfer dengan mengisi BERITA keterangan, deposit nya TIDAK akan kita proses, dan akan kita proses REFUND kembali ke rekening anda.

Untuk informasi lebih jelas, silakan hubungi LIVECHAT resmi ONGTOTO via website.

Terima Kasih, Salam Management LXGROUP.

|

|

|

|